15 min read

SB 326 Balcony Law & Reverse Mortgages: What California Seniors Must Know

Introduction

California’s SB 326 often called the “Balcony Law” was enacted in response to a series of tragic balcony...

Are you a homeowner in your 60s looking for a way to stretch your retirement income? Well, a reverse mortgage might be exactly what you need.

A reverse mortgage is essentially a type of loan that allows you to tap into the equity you’ve built in your home. Unlike a traditional loan, you’re not even required to make monthly mortgage payments.

Sounds intriguing?

Instead of paying the lender each month, the lender pays you! You then get that money as a lump sum, monthly payments, or even a line of credit to use whenever you need it most. The best part about all this is you get to stay in your home as long as it's your primary residence and you keep up with your property taxes, insurance, and basic maintenance.

Since most reverse mortgages, termed as Home Equity Conversion Mortgages (HECMs), are backed by the Federal Housing Administration (FHA), these loans are tightly regulated.

Here’s everything you need to know about reverse mortgage costs so you can decide if it’s actually what you need.

![]() A reverse mortgage allows homeowners in their 60s to borrow against their home equity.

A reverse mortgage allows homeowners in their 60s to borrow against their home equity.

![]() Home Equity Conversion Mortgages (HECMs) are the most common type that are insured by the FHA.

Home Equity Conversion Mortgages (HECMs) are the most common type that are insured by the FHA.

![]() Proprietary reverse mortgages are private loans with higher limits.

Proprietary reverse mortgages are private loans with higher limits.

![]() Reverse mortgage lines of credit offer flexible access to funds, and interest is only charged on the amount used.

Reverse mortgage lines of credit offer flexible access to funds, and interest is only charged on the amount used.

![]() Costs include origination fees, mortgage insurance premiums, servicing fees, appraisal fees, title insurance, and counseling fees.

Costs include origination fees, mortgage insurance premiums, servicing fees, appraisal fees, title insurance, and counseling fees.

![]() Loan proceeds can be received as a lump sum, monthly payments, a line of credit, or a mix of options.

Loan proceeds can be received as a lump sum, monthly payments, a line of credit, or a mix of options.

![]() Borrowers must still pay property taxes, homeowners' insurance, and maintain the home to avoid default.

Borrowers must still pay property taxes, homeowners' insurance, and maintain the home to avoid default.

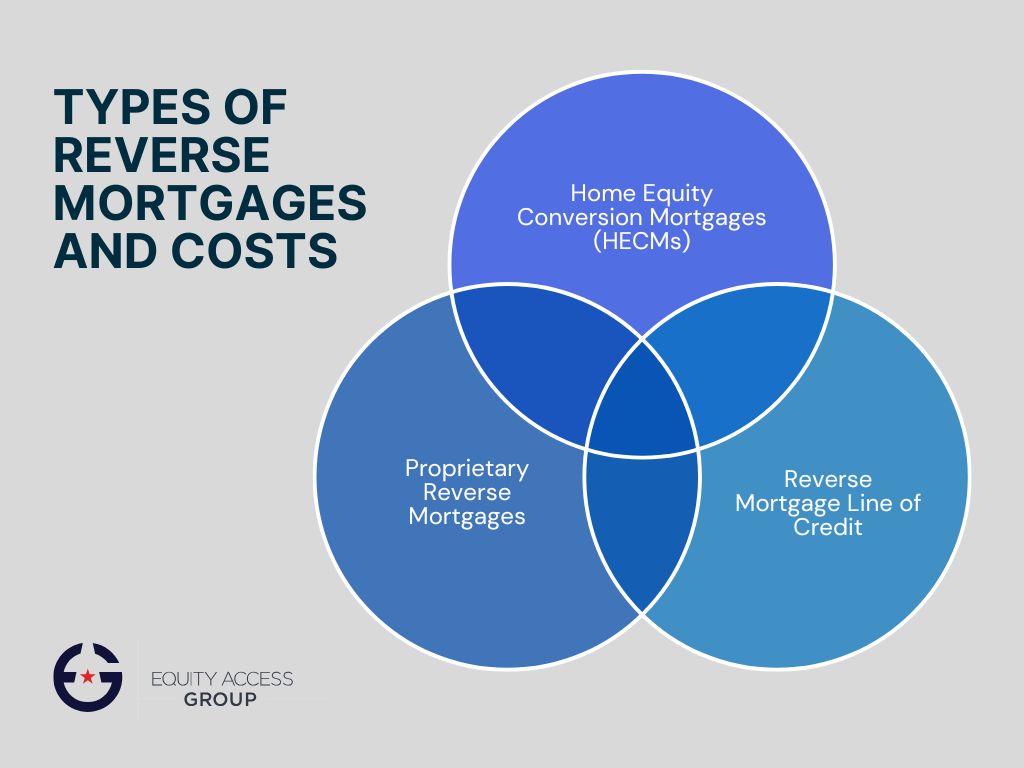

There are a few different types of reverse mortgages, each with its own features, benefits, and costs, and knowing the difference between them can come in handy.

A popular reverse mortgage is a HECM, backed by the FHA. Since they’re federally insured, they come with strict guidelines that protect borrowers.

Costs include:

HECMs are incredibly flexible. You can receive your money as a lump sum, monthly payments, or a line of credit.

Proprietary reverse mortgages are private loans usually offered by financial institutions and banks. They allow access to higher loan amounts; however, they’re not insured by the federal government.

While proprietary reverse mortgages are an attractive option, they don’t provide as much protection as HECMs. If you do end up going down this route, make sure to consult a financial advisor.

This option is a specific loan within an HECM. Funds are accessible to you as needed, and you don’t need to make monthly mortgage payments.

The reason some people go with this option is:

Before going down the reverse mortgage route, it’s important to understand that there are several built-in costs. These include:

One of the first decisions you’ll make is whether to go with a fixed interest rate or a variable rate:

Fixed-rate reverse mortgages lock in the same rate for the life of the loan. These are usually tied to lump sum payouts and give you predictability, but no flexibility to borrow more later.

Variable rates fluctuate with the market. These are more common with HECM reverse mortgages, where you’re receiving monthly payments or using a line of credit.

Regardless of the rate type, interest accrues over time. That means your loan balance grows even though you’re not making monthly payments.

Your reverse mortgage lender will charge an origination fee to process the loan. For HECM loans, this fee is regulated:

You’ll pay 2% of the first $200,000 of your home value, and 1% of anything above that.

The fee is capped at $6,000.

Some lenders may even offer lower origination fees, so always make sure to compare offers.

If you choose a Home Equity Conversion Mortgage (HECM), you’ll need to pay mortgage insurance:

This FHA insurance protects both you and the lender by guaranteeing loan payments even if your home’s value drops below the loan amount.

Many reverse mortgage lenders also charge servicing fees. This is a monthly charge to manage your loan, send statements, and make sure you're keeping up with property taxes, homeowners insurance, and home maintenance.

These fees are typically capped at $35/month, though some lenders waive them entirely.

You’ll still be responsible for paying property taxes, keeping up with homeowners' insurance, and making sure your primary residence stays in good condition.

A major advantage of a reverse mortgage is the flexibility you get in terms of your loan funds. The best part is that you get to choose from different disbursement options, based on your needs and financial goals.

A lump sum payout is the perfect option if you’re looking to get your money up front. This method comes with a fixed interest rate, which means both your loan balance and interest rate are locked in from day one.

The line of credit is a more flexible option. You simply borrow what you need, when you need it.

A line of credit comes with a variable rate, so your interest accrues based on market conditions.

Some borrowers prefer monthly mortgage payments from the lender. These payments can be:

It’s a great way to create a steady income stream during retirement.

If you’re unable to decide which method suits you best, you’ll be pleased to hear that you don’t need to stick to just one method! HECM loans allow you to mix and match options. For example, you can take a portion up front and set up a line of credit for future use.

Hear us out. Before you take out a reverse mortgage, make sure you understand exactly how the numbers work. Unlike traditional loans that most of us are used to, a reverse mortgage comes with terms you need to familiarize yourself with.

Since you’re not paying monthly mortgage payments, your interest accrues over time and gets added to your loan balance. This means that whatever amount you owe increases with time.

An outstanding mortgage balance includes:

The original loan amount

Interest

Servicing fees

Other reverse mortgage costs, such as closing costs or origination fees

Once your loan is due, usually when you’re moving out, selling the home, or pass away, the total must be repaid.

Yes, you’re borrowing against your home equity — but you still have to keep up with some very important responsibilities. This includes:

If you fail to meet these requirements, you could be at risk of default.

Total Annual Loan Cost (TALC) is a simple, standardized way of showing the full cost of a reverse mortgage over time, including interest rates, fees, and all the extras. It helps you compare offers from different reverse mortgage lenders and choose the one that fits your situation best.

As a homeowner in your 60s, a reverse mortgage can be a lifeline. It’s an ideal way to turn your home equity into cash without the need for making monthly mortgage payments and selling your home.

The money from a reverse mortgage is tax-free, and you can use it in any way you need:

To pay off medical bills or credit cards

Make home improvements

Cover everyday living costs

Or simply enjoy a little more financial breathing room in retirement

The best part about this is that you still get to keep the title of your home. Since HECM loans are backed by the FHA, you get an additional protective layer. If the loan ends up being worth more than your house later on, you don’t have to cover the difference.

You also get ample flexibility in terms of receiving your money. Whether you need to get a lump sum, monthly payments, a line of credit, or a mix of options, you have full control. Having this sort of flexibility makes it easy to plan with your options around your goals and lifestyle.

Can reverse mortgages be a smart financial move? Absolutely.

Do you need to step back and look at the bigger picture before signing anything? Absolutely.

You need to start by asking yourself some really important questions:

The good news is that you don’t have to navigate this all alone. You can get a financial advisor on board to help you out. Someone who understands your retirement planning can walk you through the potential costs, how your loan balance is likely to grow over time, and what it means for your heirs.

You need to make sure you don’t rush this process. Take your time reading the loan terms and conditions carefully, and make sure you understand the interest rates, fees, and repayment conditions. When something feels unclear, ask questions! A reverse mortgage is a long-term decision, so it’s crucial to get it right from the very beginning.

To put it frankly, a reverse mortgage isn’t something you get into without doing your homework.

Here are some common mistakes you should avoid:

Most borrowers don’t make monthly mortgage payments on a reverse mortgage. However, you’re still responsible for paying property taxes, homeowners' insurance, and maintaining the home.

The average interest rate for a reverse mortgage in 2025 ranges from 6.75% to 7.5%. However, this rate depends entirely on your lender, credit profile, and whether you choose a fixed or variable rate.

Hidden costs may include origination fees, mortgage insurance premiums, servicing fees, and appraisal or title charges.

The biggest downside is that your loan balance grows over time, which can eat away at your home equity. It may also limit what you can leave behind to your heirs.

Yes, reverse mortgage fees tend to be higher than traditional mortgages. This includes the upfront FHA mortgage insurance premium, lender origination fees, and ongoing costs like monthly insurance and servicing fees.

Total costs vary widely, but most borrowers pay between $10,000–$15,000 in upfront fees, depending on home value and loan amount.

The 95% rule means that heirs who want to keep the home can buy it for 95% of its appraised value, even if the loan balance is higher.

For many, the biggest issue of reverse mortgage is not fully understanding the long-term financial impact. While reverse mortgages offers immediate cash flow, it also reduces home equity and may complicate estate planning.

A reverse mortgage can unlock home equity, give you breathing room in your retirement plan, and get rid of those monthly mortgage payments.

But it also comes with its fair share of costs, terms, and long-term implications.

Too many borrowers jump in without understanding the loan balance, interest rates, or the fine print buried in the closing costs.

And that’s where people go wrong.

If you’re considering a reverse mortgage, don’t just Google your way through it. Talk to experts who understand this inside out.

At Equity Access Group, we help you understand not just the numbers, but the story behind them. We make sure you know exactly what you’re signing up for.

Bottom line? A reverse mortgage can absolutely work, but only if it fits your goals, your future, and your life. Get guidance that puts your interests first.